Pips and Dips for Netflix

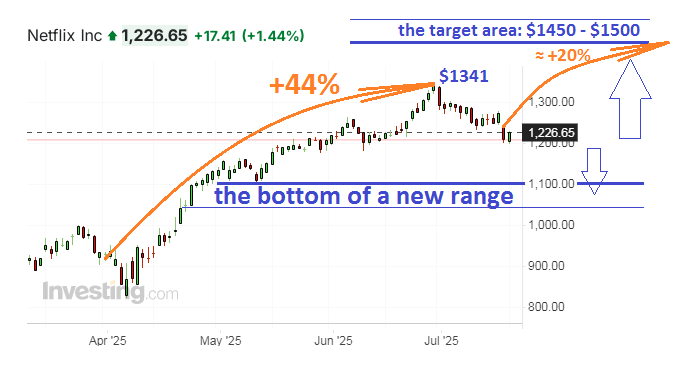

Ahead of the widely anticipated parade of tech giants, when Google, Tesla and IBM need to confirm the strength of the overall tech rally on the night before July 24, a modest quarterly release of the world's leading streaming service Netflix, with its market value of "just some" half a trillion greenbucks, released last week, went nearly unnoticed. This is quite understandable, because the Q2 figures had not much food for deep thought inside them to impress the investment community this time. If so, the market purely dropped from under the $1275 closing price on July 17 to test the $1200 area. However, this $75 initial pullback represents only 5.88% of Netflix's share price, not enough to generate active buying interest in an asset that grew from $927.50 on April 1 to an all-time high of $1341.15 by the end of June.

It went 44% up in three months, then pulled back 5% long before the Q2 report, and roughly another 5% after the report. The path behind suggests that all the clever bulls who rode the rally have done their job properly, and then took profits from their quick actions in two short waves, but overall expect this growth to continue gradually. They are simply not ready for intense action right from the current levels. This can also be judged, since the initial rebound in the beginning of the new week has been rather small so far, just within 1.5%.

I would draw my personal range of potential valuation for Netflix shares in the coming months, the bottom of which could be between $1050 and $1100. Yet, I don’t see any options or fundamental reasons for the asset to move lower. So, anything closer to $1100, if the market would give us such prices, is a basic territory for active Netflix purchases, with targets around $1450 to start with, I would say. This harvest looks modest in terms of quantity, though promising good taste if we appreciate small but easy profits in a short period of time. Again, buying any local dips in Netflix could later transform into a story when one bought near long-term lows.

After all, if the quarter before next earnings can result in just price stagnation no higher than $1450 or $1500, then the next earnings report on October 15 can boost the rally again. The only thing is that Netflix would barely cost $1100+ or $1200 at that moment. I think so because Netflix lifted its annual revenue guidance on July 17 to a higher range between $44.8 billion and $45.2 billion, thanks to "healthy member growth and ad sales" plus "weakening USD". Its previous guidance was up to $44.5 billion. Its April-to-June results topped consensus estimates as well, albeit slightly. There was no sign of weakness, that's my point! I don't like the "Squid Game" because I'm not a fan of hardcore. But the final season of this global phenomenon already helped Netflix to do math in Q2, and the streaming service's CEOs cited its effect when raising their forward guidance for the year as well. So I like the money that Netflix and I will make from this stupid story.

Yes, some part of the crowd did hope for more from the dominant movie in Q2, but Q2 diluted EPS (earnings per share) of $7.19 was only an inch higher than $7.08 in consensus forecasts. I suppose those expectations will be justified at last, after a short delay, that is, in the next two or three months, and during this time, some newer plots will do the rest of the job. "Wednesday" returns in August, and it seems to me that Tim Burton's style has an audience that does not quite match the audience of the Squid Game. So, new folks will come to pay and see. The final episodes of "Stranger Things" will be released in November and December to create extra expectations for the Christmas quarterб which always sells itself. From this, I conclude that we shouldn’t expect too deep lows, and then there may not be any explosive growth, but... before the end of the year, Netflix shares will make many small steps up. You will not notice how you will find yourself on a new peak with them.

Disclaimer:

The comments, insights, and reviews posted in this section are solely the opinions and perspectives of authors and do not represent the views or endorsements of RHC Investments or its administrators, except if explicitly indicated. RHC Investments provides a platform for users to share their thoughts on financial market news, investing strategies, and related topics. However, we do not guarantee the accuracy, completeness, or reliability of any user-generated content.

Investment Risks and Advice:

Please be aware that all investment decisions involve risks, and the information shared on metadoro.com should not be considered as financial advice. Always conduct thorough research, seek professional advice, and exercise caution when making investment decisions.

Moderation and Monitoring:

While we strive to maintain a respectful and informative environment, we cannot endorse or verify the accuracy of all user-generated content. We reserve the right to moderate, edit, or remove any comments or posts that violate our community guidelines, infringe on intellectual property rights, or contain harmful content.

Content Ownership:

By submitting content to metadoro.com, users grant RHC Investments a non-exclusive, royalty-free license to use, display, and distribute the content. Users are responsible for ensuring they have the necessary rights to share the content they post.

Community Guidelines:

To maintain a positive and respectful community, users are expected to adhere to the community guidelines of Metadoro. Any content that is misleading, offensive, or violates applicable laws and regulations will be subject to moderation or removal.

Changes to Disclaimer:

We reserve the right to update, modify, or amend this disclaimer at any time. Users are encouraged to review this disclaimer periodically to stay informed about any changes.